Bad credit but want debt consolidation? Explore expert guidance

Many people across Ireland feel trapped by mounting debts and the weight of past credit mistakes. But debt consolidation remains possible even when your credit history isn’t perfect. You might ask yourself, Can I get debt consolidation loans with bad credit? Yes, you can.

The loan brokers often become valuable allies in this situation. They know which lenders might say yes when banks say no. These finance experts work with specialised lenders who focus on helping people with credit challenges.

A good broker can match your situation with the right lending partner, rather than approaching each lender separately and facing multiple rejections. This guide walks you through options that exist beyond traditional banks.

Why Is Bad Credit a Problem for Loan Approval?

Bad credit follows you like an unwanted shadow when you’re trying to get loans. The lenders get nervous when they see poor credit scores. They worry you might not pay them back. Your past financial mistakes make them think twice about trusting you with their money. Most direct lenders check your credit history before saying yes to any loan request.

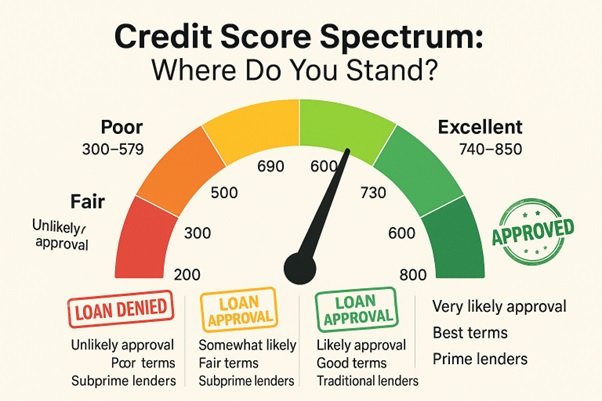

Many doors close quickly when your score drops below 580. You might hear “sorry” more often than “approved” when applying for loans. Traditional banks in Dublin, Cork, and across Ireland tend to be the most stringent on credit requirements. They have shareholders to answer to and strict lending rules to follow. Your application might get tossed aside without much consideration if your score falls short.

The lenders charge extra interest to cover the risk they’re taking on you. A financial penalty for past money mistakes. What might cost someone else 5% could cost you 12% or higher based on how low your score has fallen.

| Credit Score Ranges and Loan Approval Chances | |||

| Credit Score Range | Approval Likelihood | Expected Interest Rates | Typical Loan Terms |

|---|---|---|---|

| Below 580 | Very Difficult | 25%+ | Short terms, high fees |

| 580-619 | Challenging | 18-25% | 1-3 years, high fees |

| 620-659 | Moderate | 15-20% | 1-5 years, moderate fees |

| 660-699 | Good | 10-15% | Up to 7 years, lower fees |

| 700+ | Excellent | 5-12% | Up to 7 years, minimal fees |

Approval rates take a nosedive when your credit score drops below 600. What many don’t realise is that each rejection can make things worse. Every loan application causes a small hit to your credit score.

- Credit report mistakes sometimes cause unnecessary rejection

- Irish Credit Bureau scores differ from scoring systems

- Self-employed borrowers face extra scrutiny with bad credit

- Previous bankruptcy stays visible to lenders for 12 years

- Some lenders check your banking habits beyond credit scores

Can I Get Debt Consolidation Loans with Bad Credit?

Many lenders require a score of 660 or higher. You’ll unlock better rates and more options with this score. You’ll sit in the driver’s seat during negotiations rather than begging for approval. The lenders see you as low-risk and worthy of their best offers.

Your mailbox might even fill with pre-approved loan offers when your score is in this range. You can also contact any broker who can match you with the right lenders for your case. This will also lower your cost.

Some lenders work with scores between 580 and 660, but expect to pay more. They’ll approve you while charging higher rates to offset their perceived risk.

Direct lenders sometimes offer more flexibility than traditional banks. You can also ask a broker to find the lender. They might look at your history and savings patterns alongside your credit score.

You don’t lose hope completely if your score has tumbled below 580. Some lenders focus on helping people in tough spots. Online lenders have changed the game in recent years. Many use alternative data beyond traditional credit scores to evaluate applications.

- Your current bank might offer special rates despite poor credit

- Some brokers can help you get approval scores as low as 580

- A co-signer can help overcome credit score issues

- Secured loans using property as collateral require lower scores

- New FinTech lenders often have more flexible scoring models

How Much Will Bad Credit Increase My Loan Costs?

The interest rates jump by 5-15% compared to what people with good credit pay. This difference might seem small on paper, but it adds up to thousands over the life of a loan. A €10,000 loan might cost you an extra €3,000 or more in interest payments alone when your credit is poor.

The origination fees add another layer of expense. These upfront charges typically range from 1% to 8% of your total loan amount. With good credit, you pay 1% or even nothing. You expect to pay closer to the high end with poor credit. On a €15,000 loan, that’s up to €1,200 to process your paperwork.

You might pay €50-200 more each month than someone with excellent credit borrowing the same amount. This extra cost strains your monthly budget and makes it harder to keep up with payments. The total cost of your loan could be 30-50% higher over its lifetime.

- Late payment penalties are often higher for bad credit loans

- Some lenders charge monthly “account maintenance” fees

- Early repayment penalties are more common with subprime loans

- Hidden fees sometimes appear in the fine print of bad credit offers

- Annual percentage rates can sometimes exceed 20% for very poor credit

Will Debt Consolidation Help My Credit Score?

The lender’s hard credit check causes a small, temporary dip. This minor setback typically vanishes within a few months as you begin making regular payments.

Your score starts climbing as you build a history of on-time payments. This consistent behaviour gradually rebuilds lenders’ trust in you. Most people see their scores climb by at least 30 points within six months of responsible payment history.

One significant benefit is reducing your credit card balances. The credit utilisation improves dramatically when you pay off multiple cards with your consolidation loan. This single factor can significantly boost your score.

You should be careful about closing old accounts after paying them off. Your credit history length matters to future lenders. Accounts with positive payment histories continue helping your score for years.

- Setting up automatic payments prevents costly missed payment marks

- Keeping credit utilisation below 30% maximises score benefits

- Requesting a credit limit increase (without using it) can help ratios

- Your debt-to-income ratio improves even if your score hasn’t yet

- Some lenders offer free credit score monitoring with consolidation loans

Conclusion

Bad credit may also be an added burden on the road to debt freedom, but it is by no means impossible. You can take steps to bring yourself together now and begin your journey toward credit and wealth.

The brokers are still one of your best sources. Not only do they save your time, but they also spare your credit multiple hits when you apply in various catalogue places; they will also discover other options that you would never have found on your own. The majority of them do not charge any upfront fees but allow payment through lenders.

Ava is Editor-in-Chief at Givemyloan and is known for her deep and practical approach to modern personal finance. She has written several articles covering topics like personal loans, business loans, etc. Coming from an economics and finance background, she has worked behind the scenes to curate informative content to help borrowers identify the right loan option.

Ava’s role at Givemyloan lets her combine her interest in writing with her curiosity to explore the finance realm. She likes to be updated about what is happening in the lending industry. Most importantly, she tries to instil her knowledge in her writing in the best way possible.

She is passionate about helping borrowers look beyond the general features of a loan, i.e. about the fees and other intricate details. When she is not writing, she likes to read contemporary fiction. She is on a mission to help educate people looking for loans so that they take the right route.